The coming reckoning

Difficult policy choices, and more economic hardship, await Bangladesh

The stock of foreign exchange reserves has taken the centre stage of the economic commentaries in Bangladesh. Hardly a day passes without some reporting or punditry in the media -- mainstream and social alike -- about the “true stock” or whether, if not when, Bangladesh will “run out” of reserves.

Often missing from the discourse is an appreciation that the stock of reserves represents interactions between demands for and supplies of foreign currencies and the exchange rate -- all of which are affected by a host of reasons including government policies.

Once one starts thinking about what has been happening in the market for foreign currencies -- particularly US dollars -- in Bangladesh, the concerning conclusion that emerges is that policymakers have been postponing hard policy choices, but the reckoning is inevitable. The relevant question is not when or where the depletion of reserves will end, but how severe the reckoning -- the depreciation of the taka and the rise in interest rates -- will be.

Let’s unpack this by starting with the foreign currency market -- using the dollar interchangeably with foreign currencies for simplicity, and to reflect the fact that most of Bangladesh’s foreign currency transactions happen in dollars.

The supply of dollars comes mainly from exports earnings, remittances, and borrowing from foreigners. Foreign currency borrowing includes official loans from other countries and multilateral agencies such as the IMF, as well as private banks and businesses borrowing from foreigners for regular business transactions. Bangladeshis demand dollars to pay for imports and to service loans to foreigners.

When the demand for dollars is higher than its supply, its price rises -- that is, more taka is needed to avail each dollar. That is, taka depreciates against the dollar. Further, if taka is expected to depreciate in future, for whatever reason, then that itself triggers an increase in the current demand for dollars -- if something is set to become more expensive tomorrow, it makes sense to hoard it today.

Developing countries fear depreciation of their currencies because it makes imports -- particularly of food and oil -- more expensive, which hurts the economy generally and the vulnerable sections of the society particularly.

To prevent the currency from depreciating, the central bank supplies foreign currency from their reserve to meet the excess demand. That is, a depletion of foreign exchange reserves means there is excess demand for foreign currency at the existing exchange rate, and a depreciation pressure on the currency.

What has been happening to the demand for and supply of dollars in Bangladesh, and what do they mean for the exchange rate?

Inflation in the advanced economies started rising towards the end of 2021 on the back of loose fiscal and monetary policy as well as supply chain disruptions in the aftermath of the Covid-19 pandemic.

Russia’s invasion of Ukraine aggravated the inflationary pressure, leading to a spike in global food and energy prices in the first half of 2022. The American Federal Reserve and other advanced economy central bankers responded by raising interest rates more sharply than has been witnessed in decades. This saw the US dollar appreciating sharply in mid-2022.

Like many other oil-importing developing countries, Bangladesh was hit hard. The bill for oil and related imports in the 2021-22 financial year alone came in at around $9 billion more than previously expected.

Table 1 clearly demonstrates this by comparing current account estimates for 2021-22 in two IMF reports on Bangladesh -- one published in March 2022, before the effects of the war in Ukraine became apparent in the data, and the other published in January 2023.

Reflecting both the widening current account deficit as well as stronger dollar, like many other developing country currencies, taka too faced strong depreciation pressures.

However, taka has depreciated much more than other comparable currencies in Monsoon Asia, though not as much as in the crisis-afflicted Pakistan and Sri Lanka (Chart 1). The relatively larger depreciation of the taka owes much to the policy choices made over the past year and half.

Food and energy price shocks and depreciation pressures present vexing policy challenges. Depreciation of the currency can exacerbate the inflationary shock. The poorer and more marginalized sections of the society can be particularly hurt. So, it is understandable why Bangladeshi policymakers baulked at allowing the taka dollar exchange rate to fall.

But their policy steps were neither effective nor equitable, and ultimately made things worse.

Buffeted by the external shocks, there was a two-pronged policy response: Strict demand management; and parallel exchange rates. The first set of steps included import controls, curtailing of imports-intensive development projects, rises in the administered prices of fuel, fertilizers, gas and electricity, and steps to reduce energy demand through black outs, shorter work and school weeks and so on.

As Chart 2 shows, the demand management has been able to reduce imports over the past year. However, depreciation pressures on taka have persisted. Indeed, despite the system of complex parallel exchange rates, introduced in September 2022, to stem the depreciation by restricting foreign currency transactions, the taka price of dollar has continued to rise.

To understand the reasons, let’s think through the drivers of supply and demand for foreign currencies.

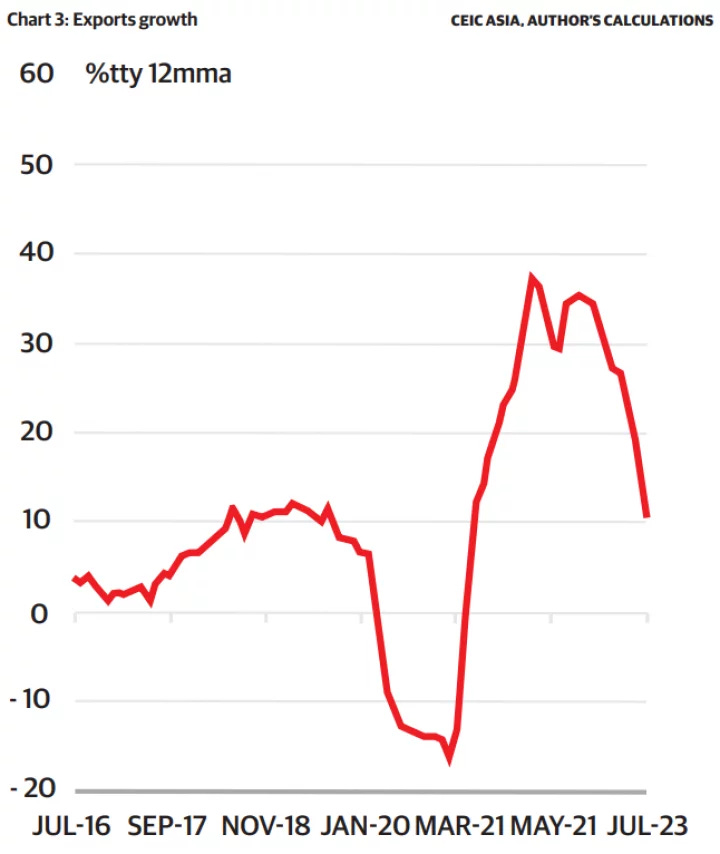

Notwithstanding the sharp rises in interest rates to curb inflation, advanced economies have thus far managed to avoid a major recession. This has resulted in Bangladesh’s exports growth remaining relatively healthy (Chart 3). However, the strong labour market conditions in the advanced economies and the Gulf countries -- destinations of most expatriate Bangladeshi workers-- have not translated into a remittances boom (Chart 4).

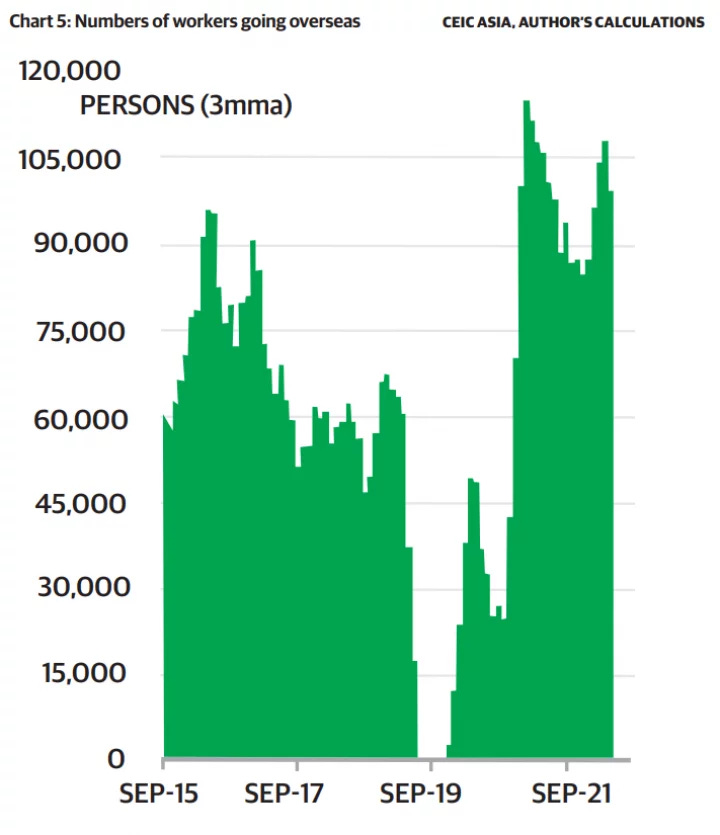

That is, while the demand for dollars has declined because of stringent restrictions, the supply of dollars has failed to match even the reduced demand because of the weakness in remittances. The lacklustre remittances performance is a particular puzzle because Bangladeshi workers are going abroad in record numbers (Chart 5).

Analysis of remittances has become difficult since the pandemic. Informal hundi channels dried up during the lockdowns and travel bans of 2020, and formal remittances growth shot up. This unwound in 2021. The more recent weakness in remittances could well be a result of the opacity around the classification of foreign reserves and confusions around parallel exchange rates.

Contrary to the internationally accepted practices, Bangladeshi authorities used to add funds that were already committed to other uses in the stock of its foreign reserves. Meanwhile, parallel exchange rates have been in effect, de facto or de jure, for different market participants since September 2022, but the central bank has never made clear their rationale, or a clear long-term vision for the exchange rate policy framework.

This lack of transparency is likely to have contributed to speculations of further depreciation of the taka, which may have dissuaded remitters from using formal channels, thereby reducing the supply of dollars. In addition, the informal hundi channels may also have been more attractive to remitters by offering more competitive rates (that is, more taka per dollar), reflecting outflows of ill-gotten wealth ahead of the election scheduled this winter.

In the meantime, even the reduction in imports have likely had adverse consequences. By disrupting the supply chains in the whole range of products, these restrictions may have driven up prices of many goods, keeping inflation elevated at near double digit rates (Chart 6).

Further, monetary policy settings have not been appropriate for an inflationary environment. With nominal deposit and lending rates capped at 6% and 9% respectively, real interest rates have been negative (Chart 7). This has buoyed aggregate demand, including demand for imports.

Of course, persistent inflation in Bangladesh even as the trading partners disinflate means taka’s purchasing power relative to other countries is declining. This is likely to be creating yet another reason to expect further depreciation of the taka.

Let’s pause and reflect

For the past year and a half, the government has been claiming that the country’s economic woes have been due to the Russia-Ukraine War. This is half-right, and therefore all wrong. Yes, the initial shocks to the economy in the first half of 2022 came from the war in Ukraine. The economic instabilities since then, however, are largely homegrown, reflecting authorities’ policy choices and mistakes.

Instead of stabilizing the economy, the policymakers have exacerbated the difficulties. The government feared inflation and thus tried to avoid depreciation of the taka. But the import restrictions, along with low interest rates, have kept inflation high. In the meantime, despite selling nearly $13bn worth of reserves, the exchange rate against the dollar is pushing 120 taka in the kerb market.

In January, the IMF assessed the government’s policy measures as “unsustainable, as they would severely suppress domestic demand to curtail imports, thus leading to disruptive macroeconomic adjustments …. are disproportionately affecting the poor and vulnerable …. and would drag medium-term growth prospects.”

The government has, nonetheless, persisted with them.

What are the alternatives?

The textbook solution to an external inflationary shock is to allow the currency to depreciate and raise the interest rate. The former might temporarily raise inflation, but the latter slows the economy, reduces the demand for imports, and stops inflation from rising further. This macroeconomic orthodoxy is the reckoning that awaits Bangladesh.

How much does the interest rate need to rise, and where might the taka dollar exchange rate settle? It is hard to be precise about these questions, but history might offer some clues.

Bangladesh experienced an inflationary episode in the early 2010s. Disinflation at that time was accompanied by a depreciation of around 17% (from around Tk70 per dollar to Tk82 per dollar) and real borrowing rates of 7-8% (nominal borrowing rate approaching 14%).

A 17% depreciation from the current kerb rates could see an exchange rate of Tk140 per dollar. From the current real borrowing rate of -2% (yes, as Chart 7 shows, the real interest rates have been negative for a while -- money is cheaper than free for those who can avail it), an early 2010s style real interest rates might mean 10 percentage point rise in borrowing rates.

Of course, these are just back of the envelope figures, and the past is never an accurate guide to the present, let alone the future. The currency has already been depreciating for a while. Interest rates are already rising. There might be a benign scenario where a much smaller rise in the interest rate and depreciation, if they are allowed to occur, stabilize the economy. However, even in this benign scenario, the adjustment process means continued inflation for a while, and an economic slowdown in 2024.

There might also be a malignant scenario of a prolonged, grinding economic slowdown. When currencies are allowed to float, they tend to suffer a bigger depreciation than might be warranted by the fundamentals -- that is, the taka could depreciate by a much larger amount.

Further, it is possible that the disruptions caused by the policy steps, coming on the heels of the pandemic, have left a lot of businesses unable to withstand higher interest rates.

Meanwhile, the country’s banking sector is in a far weaker shape now than was the case a decade ago, and even a modest rise in interest rates could put the economy on a tailspin because of banking sector woes.

That is, there could be a lot of pain ahead.

Senior officials and figures of authority have indicated that economic policies are not likely to change before the election. However, a reckoning is due, and economic forces are not beholden to political calculations and timetables.

A slightly different version was published in the Dhaka Tribune. I am indebted to comments and discussions at an online economic forum hosted by Zia Hassan. Underlying data are available upon request.

Further reading

SM Ali Abbas, Alex Pienkowski, December 2022

Another systemic debt crisis in low-income countries can be prevented – if we act now

Chuku Chuku, Guillaume Chabert, Marcos Chamon, Dalia Hakura, Jeromin Zettelmeyer, 30 May 2023

The dire situation on debt has become pressing — urgent action is needed

Martin Wolf, 14 June 2023

Banking sector’s wounds much deeper than you knew

Shaikh Abdullah, 14 Aug 2023

Global Debt Is Returning to its Rising Trend

Although global debt recorded another significant decline in 2022, it is still high, with debt sustainability remaining a concern

Vitor Gaspar, Marcos Poplawski-Ribeiro, Jiae Yoo September 13, 2023

High LC confirmation fees make imports costlier

If the average LC confirmation fee was considered 3% annually, local importers paid an additional $1.8 billion or over Tk19,000 crore in FY23

Sajjadur Rahman, 18 Sep 2023

Lessons from a century of inflation shocks

Robin Wigglesworth, 18 Sep 2023

To prevent a global catastrophe, the international community must establish mechanisms to ensure timely and fair burden-sharing among sovereign creditors

Anne Kruger, 19 Sep 2023

Banks hold $800m more in August YoY on cautious repayments

Tonmoy Modak, 24 Sep 2023

Cenbank finally moves to make money costlier to fight inflation

Reference lending rate surged to a six-month high of 7.20% as the central bank stopped money creation for the government’s deficit financing to curb money supply

Jebun Nesa Alo, 3 Oct 2023

আইএমএফের লক্ষ্যমাত্রা পূরণে আশঙ্কার মধ্যেই জুন নাগাদ ৩০ বিলিয়ন ডলারের রিজার্ভ গঠনের আশা

আবুল কাশেম , শেখ আবদুল্লাহ, সাইফুদ্দিন সাইফ & রিয়াদ হোসেন, 3 Oct 2023

'I feel hopeless': Living in Laos on the brink

Alastair McCready, 8 October 2023