Bangladesh economy in 2024 and beyond

Bangladesh economy in 2024 and beyond

A presentation on the current difficulties and possible scenarios

Greetings, acknowledgement, background, housekeeping etc.

Making these points by using a set of charts, previously published here and elsewhere. Assume familiarity with issues, but not necessarily economic jargons. 1 and 2 are reasonably well known, 3 and 4 are perhaps less so, and 5 is crystal ball stuff. Will rely on official data. Know the scepticism about BD govt data. But prefer to stick to official data to tell the story. Not because trust official data as the truth. But do think it is not as bad as is made out. And it still tells you a credible and nuanced story. Dismissing official data wholesale can actually generate more heat than light.

Don’t be fooled by precise predictions. Good economic analysis can be generally right. all economic analysis is precisely wrong.

The economy was growing at 6-8% range before the pandemic.

From the production side – steady contribution from industry (manufacturing and construction), with services varying.

From the expenditure side – strong private consumption (all years), fiscal expansion before the 2018 election, and investment (both public and private).

Strong domestic demand partly offset by negative net export, though this was somewhat unwinding in FY2019

Bangladesh became a capital importer in the late 2010s.

Savings was already high, but investment rose very strongly. Both private but also very strong public investment.

CAD is the flipside of inv>savings.

Meanwhile, BD had higher inflation than neighbours.

Was these in and of themselves a problem?

Well, if you run a CAD and have higher inflation than trading partners, then your currency should depreciate. Ours didn’t. Nor did reserve fall.

CAD was being financed by foreign borrowing. If people are willing to lend you, then is that a problem?

Remember, interest rate was low back then.

In any case, in 2019 the economy showed signs of rebalancing.

BD also had higher inflation than other countries. Late 2010s was a time of low inflation globally. Absent any global shock, BD inflation was running at 5-6%. Absent shocks, inflation is whatever the authorities allow it to be – determined by monetary and fiscal policies. Without being too technical about it, govt thought 5-6% inflation was okay. And it normally is ok – as long as you don’t have a shock.

Back in 2019, IMF AIV printed these charts. State owned banks were carrying bad loans, and were poorly capitalised. There were also governance issues around megaprojects and power plants.

Now, capital importing country with weak banking sector, governance issues – this is the story of Thailand or Indonesia of mid-1990s. For BD, things were not necessarily so bad because the capital and financial accounts were not liberalised – not so much foreign hot money coming in. but the problem of governance was definitely significant.

Plus, BD had less room to move – low taxes, RMG dependence.

The quarterly GDP has been one of the lesser publicised IMF conditions.

Contrary to conventional wisdom, published Nat Acc actually shows that covid did have the kind of impact one saw elsewhere – massive contraction during lockdown, and then recovery in 2021.

Covid had other impacts – supply chain disruptions and its impact on the firms’ and banks’ balance sheets, not to mention prices. Inflation was a surprise around the world. central banks started raising rates. Dollar was appreciating.

On top of that, extra oil import in the summer of 2022.

So, by the middle of 2022, taka was under pressure.

And this is a tricky policy problem. Want to reduce demand for dollar: can’t do anything about loan repayments, so need to curb import. Want to increase supply of dollar: can’t do much about export diversification but can increase remittances as such. Depreciation however can help both.

Depreciation also means inflation.

Tighter macro policy can offset some of the inflation.

That’s the textbook suggestion, and it is politically tough.

So, the govt tried ‘unorthodox’ – or rather, really old school – approach: direct import control. The idea was that if import is directly curbed, then the demand for dollar would decline, and there would be less pressure on exrate.

This might have worked for a while, but there were three confounding factors.

First, interest rate caps. This meant money became cheaper-than-free. This meant that the demand (including imports) didn’t slow as much. Meanwhile, import controls meant supply disruptions. These fuelled inflation.

Second, smoke and mirror around reserves, parallel exchange rate etc meant remitters were expecting depreciation, and this meant further depreciation pressure.

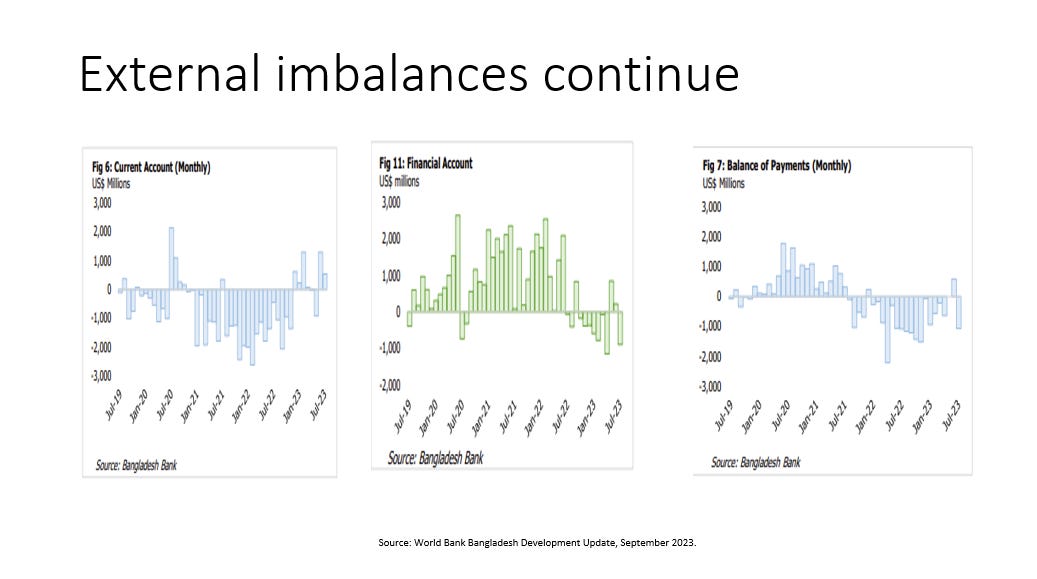

Third, financial accounts hangovers from covid disruption. Recall, CAD should mean KAS – in BD this means FAS. As CAS happens, we would expect FAD. But what happened here is that FAD happened even while CAD!

This is a WB chart, from BB data.

Times of CAD is when FAS finances the deficit. Recall savings-investment imbalance – excess investment is financed by getting money from abroad: FAS. This was the pre-covid story.

2022 CAD is higher import bill, then easy money (for a bit), plus higher inflation means people dipping into savings, for a bit. Again, CAD should be financed by FAS. But FAD from second half of 2022. This happened because of tightening of global credit market and post covid hangover plus depreciation.

Which put further pressure on reserves. Which increased expectations of depreciation. Which meant CAS isn’t as durable as could be.

Remittances stagnating, even though there are record number of people going overseas and foreign job markets are booming.

Does this mean remitters have been expecting depreciation and getting better rates through hundi?

Import control has turned NX contribution positive. This is also seen in CAS.

Domestic private demand, however, made a much smaller contribution, both investment and consumption slowed.

Look at the right hand chart – quarterly data makes it easier to see the trends, and we see that slowdown hit in 2023.

Services grew in late 2022, but then slowed in early 2023, this could be because of the high inflationary environment.

Industry is linked to exports and RMG, but even here, import control is probably having an effect.

And the overall uncertainty is hurting investment. Now, the rationale for interest rate caps was investment, and investment has slowed sharply! So, whoever borrowed this money didn’t do anything to improve the productive capacity of the economy, and their ability to repay the money is at best questionable.

So, what does that mean for the banking sector?

The inflation chart is self explanatory. The thing to note: for a while in 2022, it was the non-food inflation that was higher, and it has somewhat moderated – this is the AD story.

Explanation for the Khichuri chart — living standard of working poor have been set back by years.

These are the October IMF forecasts, before they came to dhaka – Executive Board meeting on Monday 12 Dec for the second tranche, and a detailed report.

Economy recovering on the back of strong investment – private and public. This means large CAD in the medium-term.

Public investment reflects pipeline of megaprojects. What is private investment outloook based on?

Economic growth is driven by the utilisation of the country’s abundant surplus labour. Role of RMG and remittance — well noted and quantified in the literature.

Less appreciated is that Bangladesh is not typical Asian exports-led growth story. Exports / GDP ratio is much smaller than Southeast Asia, and is dominated by RMG.

Successful Asian developers had moved beyond RMG by now. No sign of that in Bangladesh. Why?

Bangladesh still has a large pool of surplus labour — employment-population ratio is lower than Southeast Asia, as is female share of labour force.

BD remains high inflationary even in the soft landing scenario.

A fifth of revenue goes to interest expenditure — lower than India, but higher than Southeast asia. Also, look at SL and Pak — this is what a fiscal crisis looks like.

In the soft-landing scenario, the economy comes full-circle to the same set of fundamentals — good or bad — as in 2019.

Remember the fat man above: can he change?

Stefan Dercon has written that sustained economic development happens when there is an elite bargain to ‘gamble on growth’.

Naomi Hossain has written about old elite bargain of ‘never again’ after the early 1970s disasters.

The need for a new elite settlement is apparent.

Lessons from East Asia (eg Joe Studwell): education; industry policy; infrastructure.

In practice, the current elite bargain is a ‘spin dictatorship’ (Daniel Treisman and Sergei Guriev) backed by an oligarchy.

How will the current order navigate the economic shocks and domestic political transitions?

The slides were presented to a professional audience. I have also included my speaking notes.

Further reading

The metamorphosis of growth policy as circumstances change

Dani Rodrik, 12 Oct 2021

Non-Western Economic Development Requires Risk-Taking

Karl Muth, 25 Sep 2022

Economic development is a fairy tale for poor nations

Eduardo Porter, 16 Feb 2023

Asia Must Monitor Rising Corporate Debt Amid Higher Interest Rates

Thomas Helbling, Shanaka J. Peiris, Monica Petrescu, May 24, 2023

Diversification of export remains a myth, still. Here is why

Titu Datta Gupta & Jasim Uddin, 16 June 2023

Countries Can Tap Tax Potential to Finance Development Goals

Vitor Gaspar, Mario Mansour, Charles Vellutini, September 19, 2023

Asia faces one of worst economic outlooks in half a century, World Bank warns

Edward White and Mercedes Ruehl, 2 Oct 2023

Violent wage protests in Bangladesh could hit top fashion brands

Vanessa Yurkevich, 9 Nov 2023

তিন মাস ধরে ব্যাংকের বাইরে নগদ অর্থ কমছে

রোহান রাজিব, 12 Nov 2023

ডলার নেই, তারল্যও সংকটে, সংকোচনের মুখে বেসরকারি খাত

হাছান আদনান, 13 Nov 2023

ডলার সংকটে আবারো অস্থিতিশীল আলু ও চিনির বাজার

শাহাদাত বিপ্লব, 14 Nov 2023

DCs, UNOs want more funds for fuel expenses, police seek more vehicles

Abul Kashem, 21 Nov 2023